Verified digital identities provide a great way for organisations across all industries to enhance trust in who is accessing their online services. This is because these types of strong digital identities are typically issued to individuals by governments or other organisations that have conducted some level of Know Your Customer (KYC), such as banks or mobile operators.

Verified identities can then be leveraged by service providers for authentication during registration and login processes. This provides greater assurance that the digital identity belongs to a specific individual, as opposed to just creating a new username/password, or using an account from an identity provider (IdP) that does not provide strong assurance – like a social media account. The use of strong authentication with verified identities helps reduce fraud and improve customer experience.

For more details on what verified identities are available in Europe, download this white paper: Europe’s digital identity landscape.

In this blog, we look at four examples of European organisations leveraging verified identities for their online services, in Finland, Sweden, Germany and the UK.

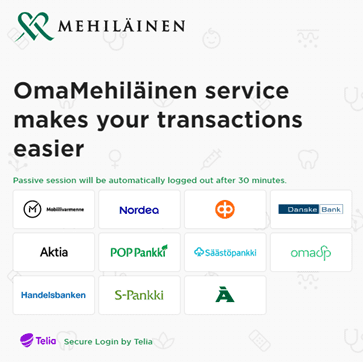

Finland: Mehiläinen (healthcare provider) and Telia Identification Broker Service

Finnish healthcare provider Mehiläinen is leveraging the Telia Identification Broker Service (TIBS) for its identity verification needs. TIBS is a platform that brings several identity providers (IdPs) under one service agreement and installation, making it very simple for the organisation (here, Mehiläinen) to enable several IdPs at once. Any additional IdPs that TIBS connects, as well as platform updates, will be automatically updated in Mehiläinen’s registration and login workflows without additional manual integration. This makes it much easier to manage on an ongoing basis, as well as the initial setup simplicity.

End users can use any of these verified identities (currently all from banks), making it a versatile and widely applicable solution. Users simply select any pre-existing account that they own from the given options (banks), securely authenticating without needing to create a new set of (unverified) login credentials.

TIBS is made possible by the Finnish Trust Network (FTN). The FTN is a framework which allows application providers to enter into a single contract, with a single integration, to make use of multiple identity providers. This Finnish scheme means that app providers don’t need to make multiple contracts for their multiple identity provider needs. Instead, app providers sign a single contract with, and integrate with, a single identity brokering service (like TIBS).

oma.mehilainen.fi

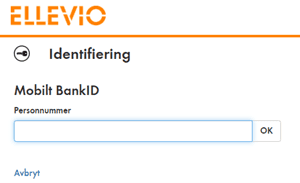

Sweden: Ellevio (energy provider) and Swedish BankID

Swedish energy provider Ellevio is benefiting from verified identities in its online service through BankID. Similar to the Finnish TIBS example, Swedish BankID offers login via several bank account options, and was an initiative developed by a number of large banks themselves.

Users begin by specifying their national ID number (as seen in the screenshot), and then continue authentication with their banking provider. The scheme estimates that it has 8 million active users, representing almost all of Sweden’s adult population, so Ellevio gets a wide-reaching identity verification solution with one integration.

www.ellevio.se

Germany: Deutsche Telekom (telco) and Verimi

Verimi is a joint venture of several German organisations for a portable identity platform between their services. The partners involved in the venture, and leveraging the platform for verified identities in their own services, are Allianz, Axel Springer, Bundesdruckerei, Daimler, Deutsche Bahn, Deutsche Bank, Deutsche Telekom, Giesecke & Devrient, Lufthansa, Samsung, and Volkswagen.

For example, German mobile operator Deutsche Telekom offers the platform for its users to strongly authentication to its online services. The end user creates their Verimi account with an email address, then stores ID card or passport data to get the full benefits of having verified their identity. They can then use this to simply log in to Deutsche Telekom’s customer portal, choosing what information they share with the service.

verimi.de/en

UK: Revolut (bank) and Onfido

In line with KYC/AML regulations, banks in the UK must verify identities. Without any applicable government-led digital identity to leverage here, banks must rely on physical ID documents to verify users during onboarding. Revolut, as a digital-first bank, leverages Onfido’s identity verification solution.

Onfido enables Revolut to see the real identities of its customers without in-person interactions. It does this by enabling a customer to submit a photo ID and selfie from their computer or smartphone. Onfido then combines the best of AI and human experts in a hybrid approach to assess if the ID is genuine, and that the photo matches the selfie.

In this way, Revolut can onboard customers worldwide digitally, with an extensive choice of physical IDs; over 4,600 document types are supported globally. This is a very useful solution for a number of sectors, regardless of country – particularly where a national-level digital ID is not available or uptake among their user base is low, such as the UK.

Onfido

Find out more about Europe’s digital identity landscape

Download your free report, looking in detail at identity in these four countries – Finland, Sweden, Germany and the UK.

The report highlights what verified identities and identity schemes are available for organisations to utilise for authentication. It also explores the advantages and disadvantages of each scheme and example use cases, and helps service providers determine the opportunities available in their region to reduce fraud and improve customer experience.

About The Author: Francesca Hobson

As Senior Marketing Manager, Francesca aims to provide valuable insights on digital identity through our Let's Talk About Digital Identity podcast, blogs, industry events and content library.

More posts by Francesca Hobson